Multiple linear regression (MLR)

Multiple Linear Regression (MLR)

- Multiple Linear Regression (MLR), also called as Multiple Regression, models the linear relationships of one continuous dependent variable by two or more continuous or categorical independent variables. If the dependent variable is measured on an ordinal scale (e.g. Likert-type scale for severity of disease), it is better to use ordinal logistic regression (ordinal regression).

- In contrast to simple linear regression, the MLR model is useful when there are multiple independent variables, as it estimates an individual slope of the regression line for each independent variable.

- If we have n independent variables (

X), the MLR model for predicting the dependent variable (y) can be represented as,

- MLR makes similar assumptions as simple linear regression. In addition, there should be no multicollinearity among the independent variables.

Note: Dependent variable also called a response, outcome, regressand, criterion, or endogenous variable. Independent variable also called explanatory, [covariates](what-is-covariate.html), predictor, regressor, or exogenous variable.

Perform Multiple Linear Regression (MLR) in Python

- For performing the MLR, we will use the plant species richness data to study the influence of different physiographic factors on the native plant richness of islands. The data is collected from 22 different coastal islands (McMaster 2005).

- The dataset contains native plant richness as dependent variable (

y) and area, latitude, and distance from mainlands as independent variables (X). - We will use statsmodels and

bioinfokit v1.0.8or later for performing MLR in Python (check how to install Python packages)

Note: If you have your own dataset, you should import it as a pandas dataframe. Learn how to import data using pandas

Let’s perform MLR in Python

import pandas as pd

import numpy as np

import statsmodels.api as sm

from statsmodels.tools.eval_measures import rmse

from bioinfokit.analys import get_data, stat

from statsmodels.stats.outliers_influence import variance_inflation_factor

# load data

df = get_data('plant_richness').data

df.head(2)

# output

ntv_rich area latitude dist_mainland

0 1.897627 1.602060 42.99 10.0

1 1.633468 0.477121 41.25 0.3

X = df[['area', 'latitude', 'dist_mainland']] # independent variables

y = df['ntv_rich'] # dependent variables

# to get intercept -- this is optional

X = sm.add_constant(X)

# fit the regression model

reg = sm.OLS(y, X).fit()

reg.summary()

# output

OLS Regression Results

==============================================================================

Dep. Variable: ntv_rich R-squared: 0.915

Model: OLS Adj. R-squared: 0.901

Method: Least Squares F-statistic: 64.98

Date: Sat, 30 Jan 2021 Prob (F-statistic): 7.47e-10

Time: 00:12:26 Log-Likelihood: 11.874

No. Observations: 22 AIC: -15.75

Df Residuals: 18 BIC: -11.38

Df Model: 3

Covariance Type: nonrobust

=================================================================================

coef std err t P>|t| [0.025 0.975]

---------------------------------------------------------------------------------

const 5.1045 0.981 5.201 0.000 3.043 7.166

area 0.3497 0.027 12.828 0.000 0.292 0.407

latitude -0.0863 0.023 -3.777 0.001 -0.134 -0.038

dist_mainland -0.0047 0.003 -1.732 0.100 -0.010 0.001

==============================================================================

Omnibus: 2.723 Durbin-Watson: 1.651

Prob(Omnibus): 0.256 Jarque-Bera (JB): 1.253

Skew: 0.130 Prob(JB): 0.534

Kurtosis: 1.860 Cond. No. 1.36e+03

==============================================================================

# regression metrics

res= stat()

res.reg_metric(y=np.array(y), yhat=np.array(reg.predict(X)), resid=np.array(reg.resid))

res.reg_metric_df

Metrics Value

0 Root Mean Square Error (RMSE) 0.1410

1 Mean Squared Error (MSE) 0.0199

2 Mean Absolute Error (MAE) 0.1227

3 Mean Absolute Percentage Error (MAPE) 0.0625

# Variance Inflation Factor (VIF)

# make sure you have added intercept (constant) in X using add_constant(X)

pd.DataFrame({'variables':X.columns[1:], 'VIF':[variance_inflation_factor(X.values, i+1) for i in range(len(X.columns[1:]))]})

# output

variables VIF

0 area 1.035192

1 latitude 1.023562

2 dist_mainland 1.026738

Jupyter python notebook: ![]()

Perform Multiple Linear Regression (MLR) in R

Jupyter R notebook: ![]()

Multiple Linear Regression (MLR) interpretation

Regression line

- The regression line with equation [

y = 5.1045 + (0.3497*area) + (-0.0863*latitude) + (-0.0047*dist_mainland)], is helpful to predict the value of the dependent variable (y) from the given value of the independent variables (X). - Regression can be useful in predicting the

yof any value within the range ofX. It also predictsyfromXoutside the given range, but such extrapolation may not be useful.

Root Mean Square Error (RMSE), Mean squared error (MSE), Mean absolute error (MAE), and Mean absolute percent error (MAPE)

- RMSE (0.14) represents the standard deviation of the residuals. It gives an estimate of the spread of observed data points across the predicted regression line. The lower the RMSE, the better is the regression model.

- Mean squared error (MSE) is the mean of the square of residuals. RMSE is a squared root of the MSE.

- Mean absolute error (MAE) represents the mean of absolute differences between actual and predicted values.

- Mean absolute percent error (MAPE) represents the mean of absolute percent differences between actual and predicted values.

Regression coefficients (slope) and constant (y-intercept)

- The regression coefficients or slope (0.34, -0.08, and -0.0047) represent the change in the

yper unit change in theXvariable after adjusting for the simultaneous linear change. It means the valueyincreases by 0.34 (slope forarea) with each unit increase inareaafter adjusting for the simultaneous linear change inlatitudeanddist_mainland. - Similarly, the value

ydecreases by -0.08 with each unit increase inlatitudeafter adjusting for the simultaneous linear change inareaanddist_mainland.Note: There is common practice to interpret the regression coefficients as a change in `y` when other `X` variables are remain constant. This may not be right. Read the full paper from Dr. David C Hoaglin for more details.

- The regression coefficients should be interpreted confidently only if they are statistically significant (p < 0.05).

- The y-intercept (5.10) represents the value of y when all X variables have a value of 0.

- y-intercept should be interpreted cautiously as sometimes the value

Xdoes not make any sense (e.g. speed of car or height of the person). In such cases, the values within the range of X should be considered to interpret the y-intercept. - The p values associated with

areaandlatitudeare significant (p < 0.05). It suggests thatareaandlatitudesignificantly influence the native plant richness.

ANOVA

- In regression, the ANOVA tests the null hypothesis that there is no relationship between the independent variable (

X) and dependent (y) variable i.e. it tests the null hypothesis that regression coefficients equal to zero (b1= b2=…=bn=0). - From ANOVA F test, the p value is significant (<0.05),

which suggests that there is a significant relationship between

Xandy. The independent variables (X) can reliably predict the dependent (y) variable.

Coefficient of determination (R-Squared and adjusted R-Squared)

- The coefficient of determination (R-Squared) is 0.91 (~91%), which suggests that ~91% of the variance in

ycan be explained by X variables. - In MLR, adjusted R-Squared (corrected for sample size and regression coefficients) is more appropriate than

R-Squared as an increasing number of

Xvariables also increases R-Squared. Adjusted R-Squared is always lower than the R-Squared. - Generally, high R-Squared or adjusted R-Squared represents better model, but it is not always true and should be cautiously used for model evaluation based on subject area.

- There is no good cut-off value of R-Squared for good model selection. R-Squared should be evaluated based on field data type, data transformations, or based on subject area decisions. For example, for the nonstationary time series dependent variable, the higher R-Squared (close to 1) may not be good.

Multicollinearity and Variance inflation factor (VIF)

- Multicollinearity (the significant correlation among the

Xvariables) is often a problem. Multicollinearity results in an inflation of variance and, changes in the signs and confidence intervals of regression coefficients (Ryan, 2008). - Therefore, it is necessary to detect and eliminate multicollinearity. Multicollinearity can be detected using correlation analysis or Variance inflation factor (VIF).

- Generally, VIF > 5 or > 10 suggests multicollinearity. But this is not a universal agreement and VIF < 5 could also suggest the multicollinearity. .

- VIF < 2 is a good indicator of the absence of strong multicollinearity and VIF = 1 indicates a complete absence of

multicollinearity. In the above results, the VIF for all the

Xvariables < 2 and suggests there is no strong relationship between the X variables. - A correlation coefficient > 0.5 among the X variables can be used to detect the multicollinearity (Vatcheva et al., 2016).

- To remove the multicollinearity you can either take more measurements or remove the variables causing multicollinearity or perform the ridge regression (Ryan, 2008).

Check Multiple Linear Regression (MLR) Assumptions

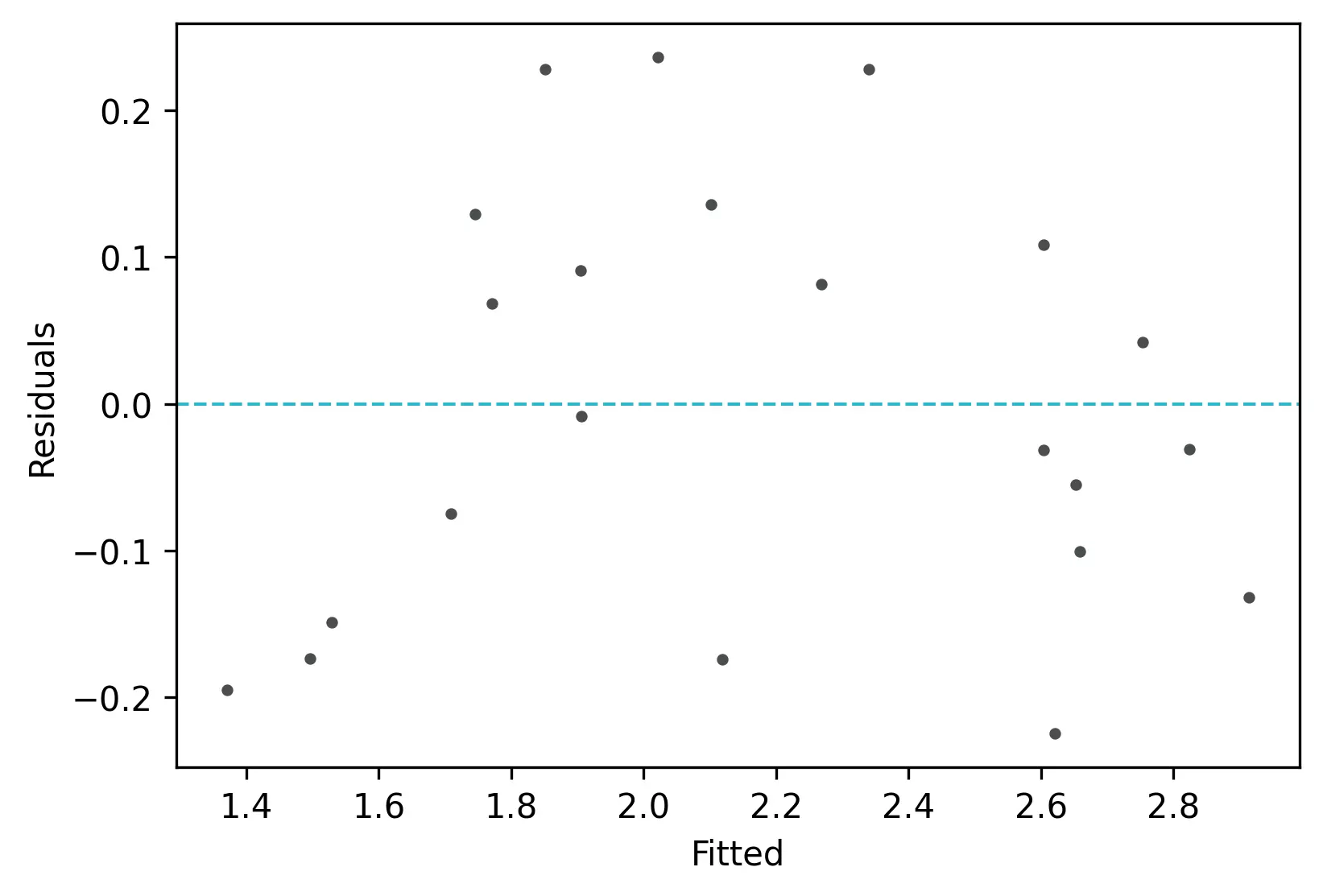

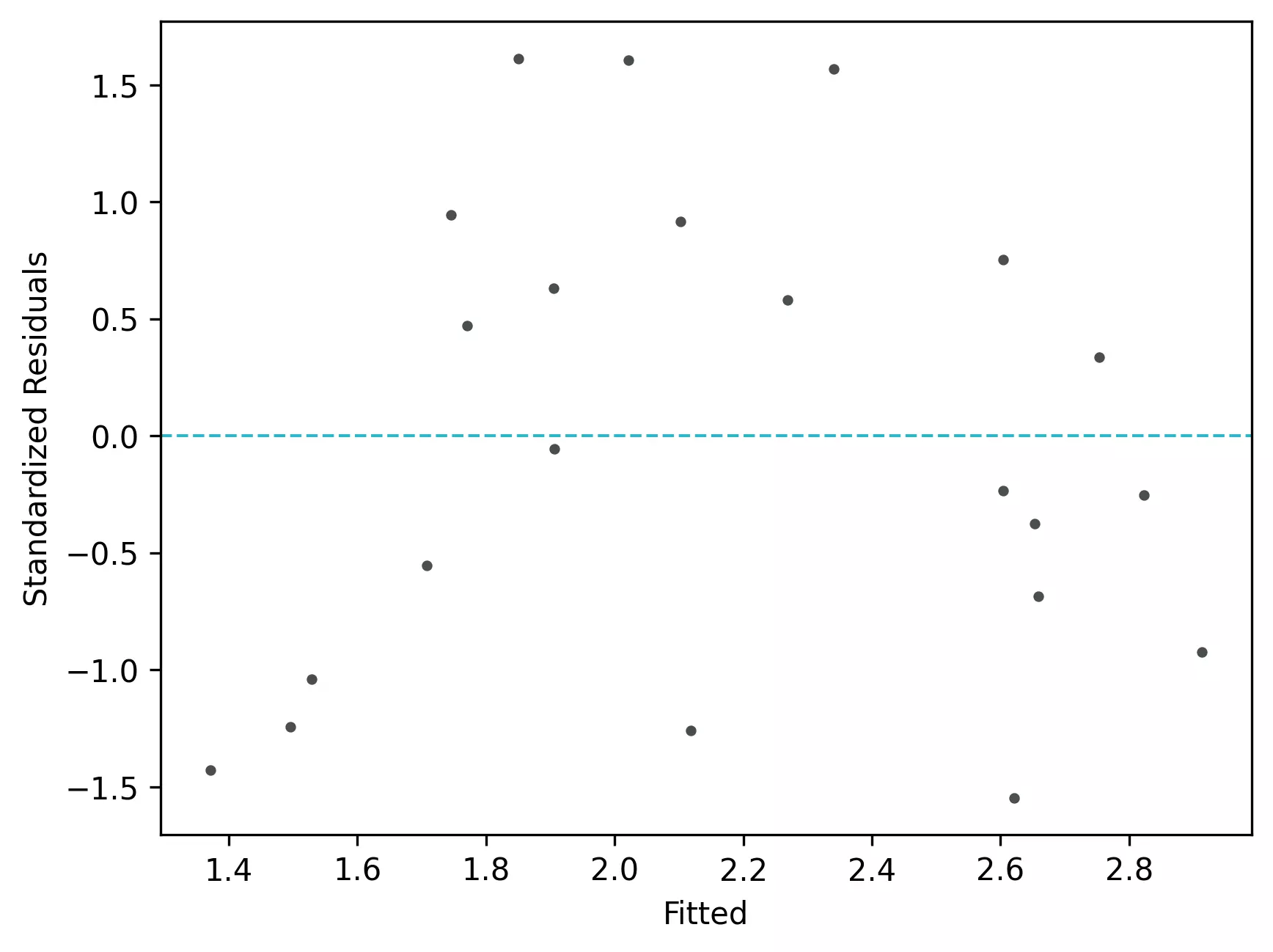

Residuals vs fitted (y_hat) plot: This plot used to check for linearity, variances and outliers in the regression data

# get residuals and standardized residuals

from bioinfokit.visuz import stat

df[['yhat']]=pd.DataFrame(reg.predict(X))

df['res']=pd.DataFrame(reg.resid)

df['std_res']=reg.get_influence().resid_studentized_internal

df.head(2)

ntv_rich area latitude dist_mainland yhat res std_res

0 1.897627 1.602060 42.99 10.0 1.906057 -0.00843 -0.056140

1 1.633468 0.477121 41.25 0.3 1.708459 -0.07499 -0.555013

# create fitted (y_hat) vs residuals plot

stat.reg_resid_plot(df=df, yhat='yhat', resid='res', stdresid='std_res')

# plot will be saved in same dir (resid_plot.png and std_resid_plot.png)

From the plot,

- As the data is pretty equally distributed around the line=0 in the residual plot, it meets the assumption of residual equal variances. The outliers could be detected here if the data lies far away from the line=0.

- In the standardized residual plot, there is no strong visible pattern and data randomly spread around the line. It suggests that it meets assumptions of linearity.

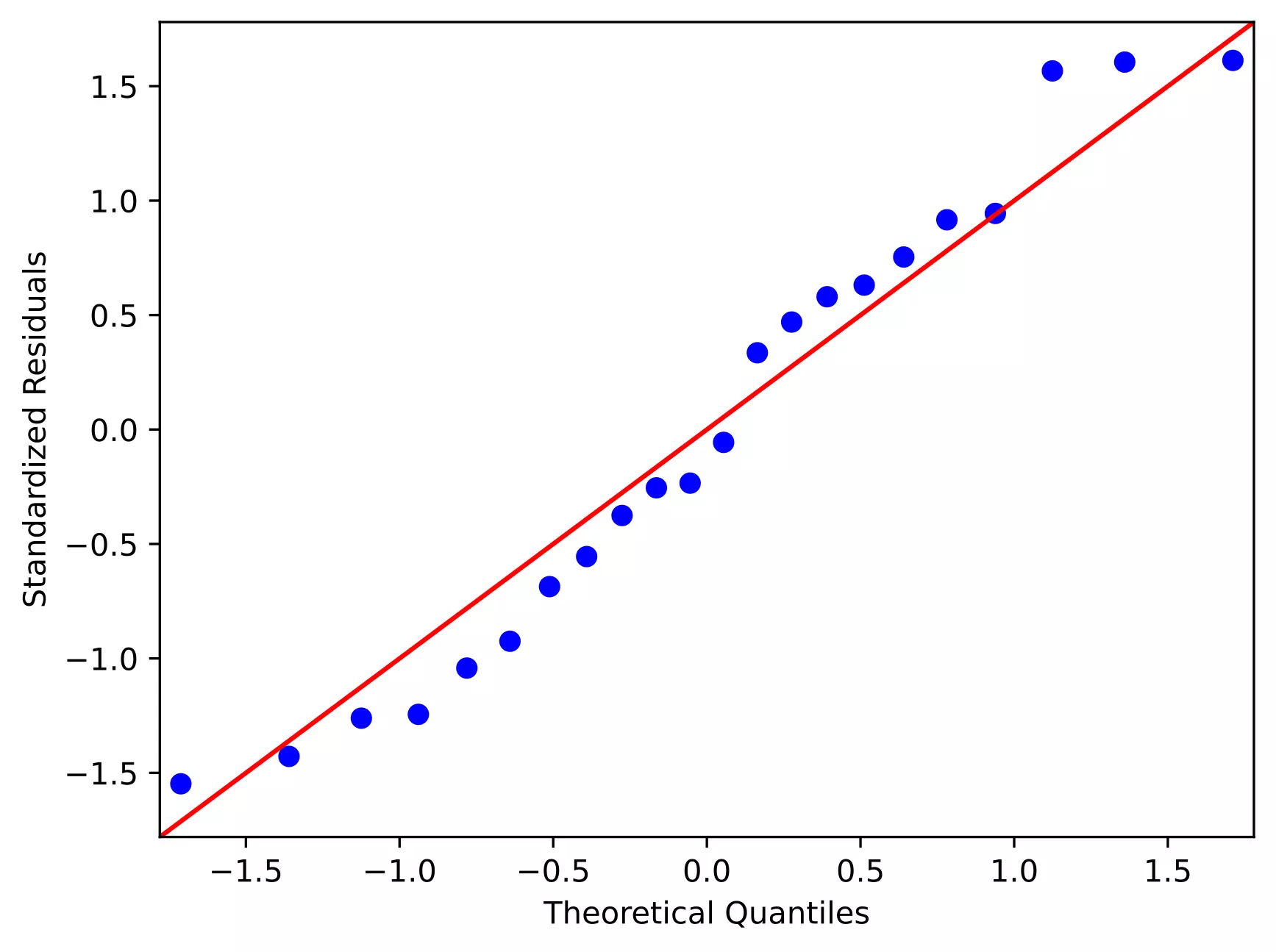

Quantile-quantile (QQ) plot: This plot used to check the data normality assumption

# python

import statsmodels.api as sm

import matplotlib.pyplot as plt

# line=45 option to plot the data around 45 degree line

sm.qqplot(df['std_res'], line='45')

plt.xlabel("Theoretical Quantiles")

plt.ylabel("Standardized Residuals")

plt.show()

From the plot,

- As the standardized residuals lie around the 45-degree line, it suggests that the residuals are normally distributed

Enhance your skills with courses on regression

- Machine Learning Specialization

- Linear Regression and Modeling

- Machine Learning: Regression

- Machine Learning with Python

Related reading

- Durbin-Watson (DW) test (with R code)

- Multiple linear regression (MLR)

- Mixed ANOVA using Python and R (with examples)

- Repeated Measures ANOVA using Python and R (with examples)

- Multiple hypothesis testing problem in Bioinformatics

References

- Vatcheva KP, Lee M, McCormick JB, Rahbar MH. Multicollinearity in regression analyses conducted in epidemiologic studies.

Epidemiology (Sunnyvale, Calif.). 2016 Apr;6(2). - Ryan TP. Modern regression methods. John Wiley & Sons; 2008 Nov 10.

- McMaster RT. Factors influencing vascular plant diversity on 22 islands off the coast of eastern North America. Journal of Biogeography. 2005 Mar;32(3):475-92.

- https://people.duke.edu/~rnau/rsquared.htm#punchline

- Hoaglin DC. Regressions are commonly misinterpreted. The Stata Journal. 2016 Mar;16(1):5-22.

If you have any questions, comments or recommendations, please email me at reneshbe@gmail.com

This work is licensed under a Creative Commons Attribution 4.0 International License

Some of the links on this page may be affiliate links, which means we may get an affiliate commission on a valid purchase. The retailer will pay the commission at no additional cost to you.